Cryptocurrency (crypto) has been growing in popularity for some time. Last year crypto, defined as the class of digital assets you can spend and invest, reached a milestone.

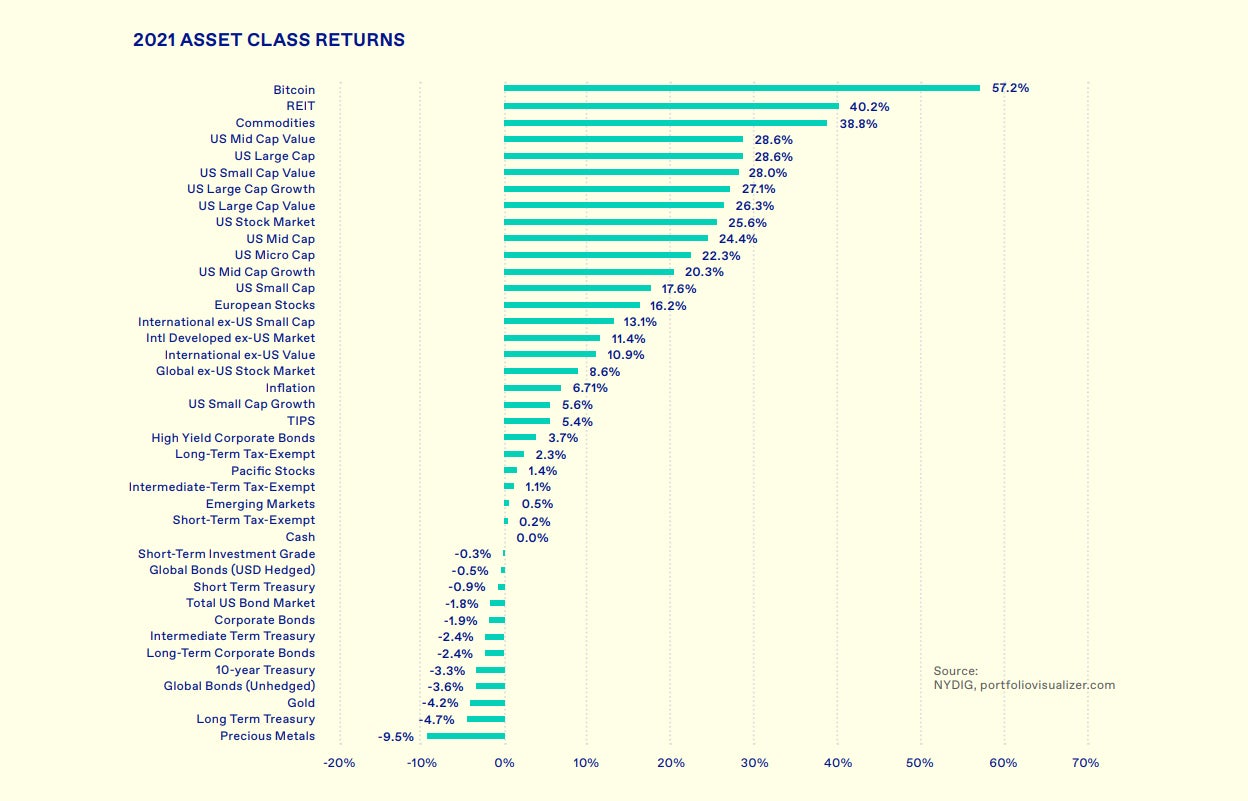

Bitcoin, the best-known crypto, had the highest investment return of any asset class in 2021, outpacing the stock market, real estate, commodities and more. It has also experienced some of the biggest price drops in January 2022. Little wonder that the media is increasingly filled with stories of crypto companies growing and investors getting rich—and going broke.

Cryptocurrencies are increasingly becoming a part of the financial services landscape for payments. More and more banks and payment networks, including Visa and Mastercard, are adopting cryptocurrency. They’re allowing consumers to use it as a method of payment and to buy it on cryptocurrency exchanges as an investment.

The U.S. Federal Reserve is also studying the potential uses of digital currencies. In conjunction with the Massachusetts Institute of Technology, the U.S. central bank is looking to see how it could issue a digital version of the dollar—and whether it should. Recently, the Fed released its report seeking more discussion and leaving a final decision to Congress.

The message is clear: Cryptocurrency is here to stay, and the financial industry knows it.

What is Cryptocurrency and How Does it Work?

Just over 10 years old, Bitcoin is the oldest and largest of the digital assets in use today. The primary distinguishing characteristic of a cryptocurrency lies in the name itself.

Cryptocurrency is a combination of cryptography and currency. The word “cryptography” is derived from the Greek root word, kryptos, (hidden) and graphy, (a form of drawing and/or writing). Bitcoin and other digital assets are written as code.

The second characteristic of a digital asset lies in how they are issued and managed. They are decentralized, meaning that no one institution—government or bank—issues and maintains the currency.

Bitcoin and other digital currencies are not controlled by any governmental agency. There is no federal institution that prints or mints bitcoins–instead, bitcoins are issued and tracked (mined) using specially built, high-powered computers that run bitcoin’s software and maintain a distributed accounting network.

The accounting ledger uses a new technology called blockchain to track currencies and ensure trust like a bank does for your checking account. However, the ledger is global and transactions are final. If you make a mistake and pay the wrong person, you cannot appeal to an authority to make good on errors.

Banks and Crypto

Given the benefits to investors and the increasing adoption, cryptocurrency isn’t going anywhere. It’s here to stay and growing in popularity among consumers looking for investments that pay big and money transfer solutions that cost little to nothing.

As a result, traditional banks are looking at how to safely embrace cryptocurrency solutions and incorporate them into their operations. Not only is it something an increasing number of consumers want, but cryptocurrency could help banks streamline and enhance their financial services. Look this year for increasing guidance on crypto from financial regulators, including the Fed, the Securities and Exchange Commission, and the Office of the Comptroller of the Currency (OCC). When commenting on cryptocurrency and the need for banks to embrace digital currency, Brian Brooks, former head of the OCC, put it like this:

“Like other technology developments in the past, there was the potential for criminal activity…There’s also an enormous potential for economic growth. So we don’t want to throw out those advantages because there’s a chance for criminal activity. Instead, we want to give compliance guidance to help banks innovate.”

Going forward, banks may see cryptocurrency providers as partners. Cryptocurrency has a lot to offer, and depending upon the regulatory requirements, banks could play a central role in ushering in a new generation of payments and investments in a way that benefits consumers while providing additional safety.

Reference: www.aba.com/member-tools/industry-solutions/insights/how-cryptocurrencies-may-impact-the-banking-industry

Source: 2021 in Review and a Look Ahead, NYDIG, January 2022